Chapter 20 - Notes

20.1 - The Full Model (IS-MP-PC)

Putting It All Together

- The full model combines three tools from the last two chapters:

- MP curve → determines the real interest rate

- IS curve → uses the real interest rate to determine the output gap

- Phillips curve → uses the output gap to determine inflation

The chain: Real interest rate → Output gap → Inflation

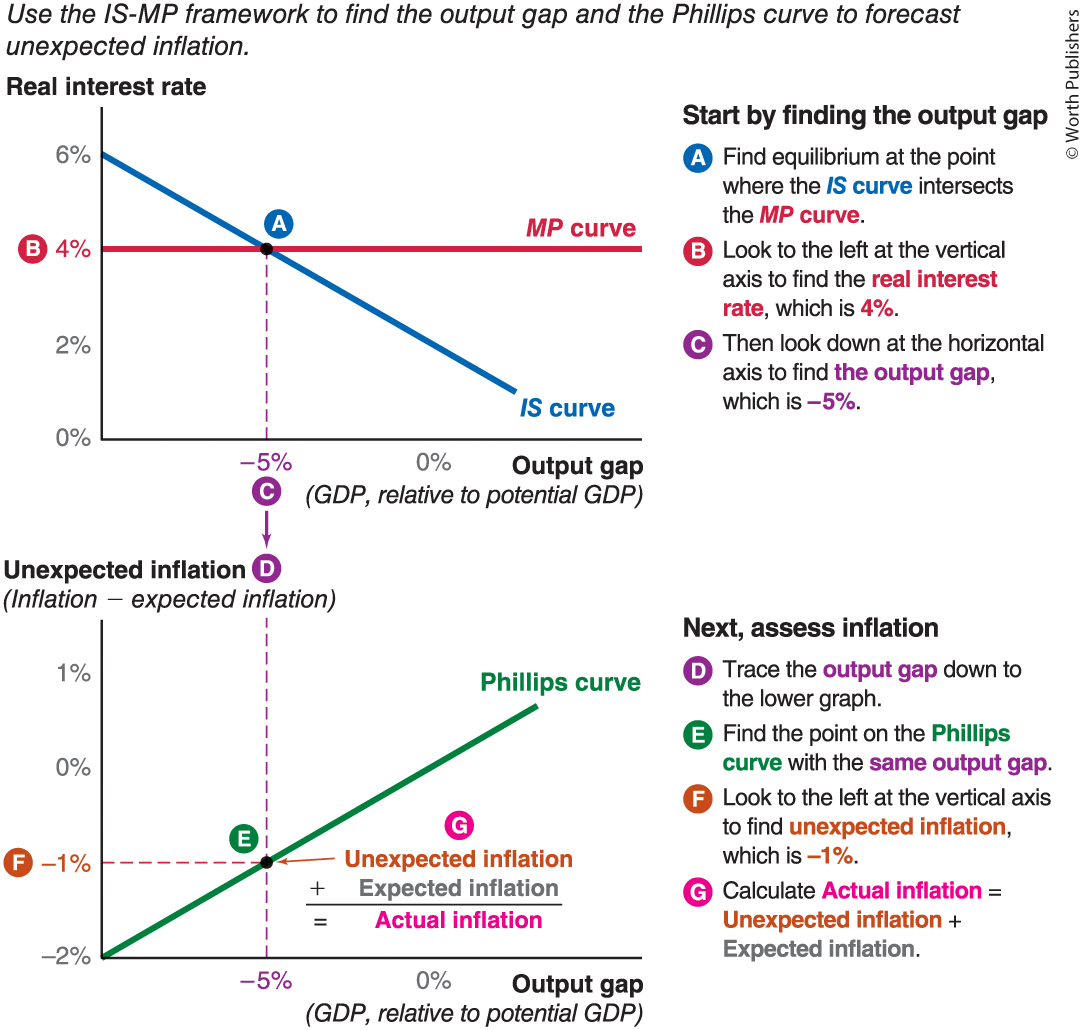

How to Forecast Using the Full Model (Step by Step)

Step 1: Find the output gap

- Use the IS-MP framework (top panel)

- Where MP crosses IS → look down to find the output gap

- e.g., MP at r = 4% intersects IS at output gap = −5%

Step 2: Assess inflation

- Take the output gap from Step 1 and plug it into the Phillips curve (bottom panel)

- Find output gap on horizontal axis → read up to Phillips curve → read across for unexpected inflation

- Actual inflation = Inflation expectations + Unexpected inflation

- e.g., output gap = −5% → unexpected inflation = −1% → if expectations = 2% → actual inflation = 2% + (−1%) = 1%

Full forecast from the example: r = 4%, output gap = −5%, inflation = 1%

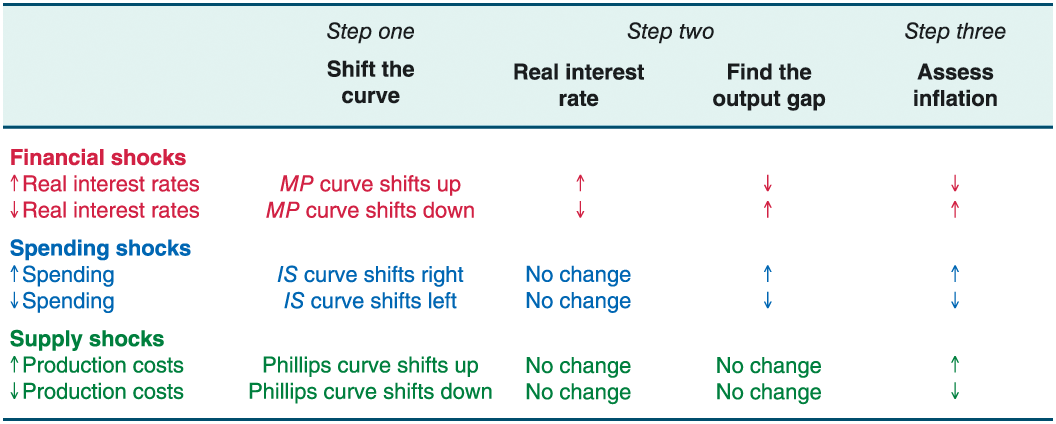

Three Types of Macroeconomic Shocks

Every possible economic event falls into one of three categories:

1. Financial Shocks → Shift the MP curve

- Bank of Canada changes the policy interest rate

- Risk premium changes due to financial market conditions

- e.g., banking crisis, Bank of Canada rate cut, rising risk aversion

2. Spending Shocks → Shift the IS curve

- Any change in C, I, G, or NX at a given interest rate and income level

- e.g., consumer confidence crashes, government increases spending, exports collapse, stock market boom increases wealth

3. Supply Shocks → Shift the Phillips curve

- Any unexpected change in production costs

- Three types: input prices, productivity, exchange rates

- e.g., oil price spike, wage-price spiral, Canadian dollar depreciates, productivity slowdown

Summary Framework:

| Shock type | What shifts | Determines |

|---|---|---|

| Financial shock | MP curve | Real interest rate |

| Spending shock | IS curve | Output gap |

| Supply shock | Phillips curve | Inflation (relative to expectations) |

20.2 - Analyzing Macroeconomic Shock

Three-Step Recipe for Any Shock

- Identify the shock and shift the curve — is it financial (MP), spending (IS), or supply (Phillips)?

- Find the output gap — look at the intersection of the (new) IS and MP curves

- Assess inflation — trace the output gap down to the (potentially shifted) Phillips curve, read unexpected inflation, add inflation expectations

Results Summary Table — Memorize This Pattern

| Shock type | Curve | Dire-ction | Real interest rate | Output gap | Inflation |

|---|---|---|---|---|---|

| Adverse financial shock | MP shifts UP | ↑ | ↑ Higher | More negative | Lower |

| Positive financial shock | MP shifts DOWN | ↓ | ↓ Lower | More positive | Higher |

| Negative spending shock | IS shifts LEFT | ← | Unchanged | More negative | Lower |

| Positive spending shock | IS shifts RIGHT | → | Unchanged | More positive | Higher |

| Adverse supply shock | Phillips shifts UP | ↑ | Unchanged | Unchanged | Higher |

| Positive supply shock | Phillips shifts DOWN | ↓ | Unchanged | Unchanged | Lower |

Key Patterns to Notice:

- Financial shocks (MP): all three variables change — r, output gap, AND inflation

- Spending shocks (IS): output gap and inflation change, but r stays the same

- Supply shocks (Phillips): ONLY inflation changes — r and output gap are unchanged (because IS and MP don't shift)

Analyzing Financial Shocks (MP Shifts)

- MP shifts when: Bank of Canada changes the policy rate, OR the risk premium changes

- Example: risk premium rises by 2% → MP shifts up → new IS-MP intersection at lower output → trace to Phillips curve → lower inflation

- Chain: ↑r → ↓spending → ↓output → ↓inflation

Analyzing Spending Shocks (IS Shifts)

- IS shifts when: any component of AE (C, I, G, NX) changes at a given interest rate

- IS shifts by: ΔSpending × Multiplier

- e.g., spending falls by $50B, multiplier = 2 → IS shifts left by $100B

- Example: AE falls by $100B (5% of potential output) → IS shifts left → output gap = −5% → unexpected inflation = −1% → actual inflation falls

- Chain: ↓spending → ↓output → ↓inflation (r unchanged)

Analyzing Supply Shocks (Phillips Shifts)

- Phillips shifts when: unexpected change in input prices, productivity, or exchange rates

- Example: production costs rise → Phillips shifts up → output gap unchanged (IS and MP didn't move) → but inflation rises

- Chain: ↑costs → ↑inflation (r and output gap unchanged)

Important caveat — Stagflation:

- Supply shocks can ALSO reduce actual output AND potential output (not just raise inflation)

- e.g., oil prices double → energy-intensive factories become unprofitable → close down → both actual and potential output fall

- This doesn't show up as a change in the output gap (both numerator and denominator fall)

- Stagflation = economic stagnation + high inflation simultaneously

- This is why supply shocks are the nastiest type — you get higher inflation AND lower output

Practice Scenarios (know the pattern for each):

- Consumer confidence rises → IS right → unchanged r, higher output, higher inflation

- Bank of Canada cuts rates → MP down → lower r, higher output, higher inflation

- Port congestion raises shipping costs → Phillips up → unchanged r, unchanged output, higher inflation

- New tech boosts productivity → Phillips down → unchanged r, unchanged output, lower inflation

- Investment collapses → IS left → unchanged r, lower output, lower inflation

- Banks raise risk premium → MP up → higher r, lower output, lower inflation

- Government cuts spending → IS left → unchanged r, lower output, lower inflation

- Banks lower risk premium → MP down → lower r, higher output, higher inflation

- Fracking lowers energy prices → Phillips down → unchanged r, unchanged output, lower inflation

- China growth boosts demand for Canadian exports → IS right → unchanged r, higher output, higher inflation

- Workers' wages fall unexpectedly → Phillips down → unchanged r, unchanged output, lower inflation

- Bank of Canada raises rates → MP up → higher r, lower output, lower inflation

20.3 - Diagnosing the Causes of Macroeconomic Changes

The Key Idea: Work the Full Model in Reverse

- Instead of starting with a shock and predicting outcomes (left to right), you observe the outcomes and diagnose the shock (right to left)

- Each type of shock leaves a unique pattern of footprints — use these to identify what hit the economy

Three Diagnostic Rule

1. If the real interest rate changed → Financial shock (MP shifted)

- Only financial shocks (monetary policy or risk premium changes) move the interest rate

- Spending and supply shocks leave the interest rate unchanged

2. If the output gap shifted but the interest rate didn't move much → Spending shock (IS shifted)

- Something changed in C, I, G, or NX at a given interest rate

- Output moves but interest rate stays put = classic spending shock fingerprint

3. If inflation and output move in opposite directions → Supply shock (Phillips shifted)

- Inflation rising in a weak economy (or falling in a strong economy) can't be explained by demand-pull

- Demand-pull always moves output and inflation in the SAME direction

- So if they move in OPPOSITE directions, the Phillips curve must have shifted

Practice Diagnostic Examples

"Inflation is falling even though the economy is strong"

- Inflation and output moving in opposite directions → supply shock

- Diagnosis: positive supply shock → Phillips curve shifted DOWN (falling production costs → lower inflation even with a healthy economy)

"Output is booming but we haven't cut interest rates"

- Output rising + interest rate unchanged → spending shock

- Diagnosis: positive spending shock → IS curve shifted RIGHT (higher AE at the same interest rate)

"Sales and output are falling, and interest rates on auto loans are higher even though the Bank of Canada didn't change its rate"

- Output falling + interest rate rising + Bank of Canada didn't act → financial shock from the risk premium

- Diagnosis: adverse financial shock → risk premium rose → MP curve shifted UP (higher rates came from financial markets, not the Bank)