Chapter 13 - Notes

13.1 - Consumption, Saving, and Income

Key Definitions

- Consumption: household spending on final goods and services — largest component of GDP (over 3/5 of total spending)

- Includes food, rent, clothes, cars, etc. — everything except buying a new home (that's investment)

- Saving: the portion of income you set aside rather than spending on consumption

- Dissaving: when consumption exceeds income (negative saving) — funded by borrowing or withdrawing from savings

- Net wealth: the amount by which your assets exceed your debts — saving increases it, dissaving decreases it

The Consumption Function

- Shows the relationship between consumption and income

- Upward-sloping — higher income leads to higher consumption

- Marginal propensity to consume (MPC): the fraction of each extra dollar of income that households spend on consumption

- MPC =

- Between 0 and 1 for most people (you spend some and save some)

- MPC = 1 means you spend all extra income, MPC = 0 means you save all of it

- MPC is the slope of the consumption function

- e.g., if MPC = 0.6, a $10 billion increase in income → $6 billion rise in consumption

- MPC =

Consumption and Saving Are Two Sides of the Same Coin

- Income = Consumption + Saving

- Every dollar you don't spend is saved, every dollar you don't save is spent

- Saving is important micro (builds your wealth) and macro (funds investment through the financial sector)

Additional

13.2 - The Micro Foundations of Consumption

The Rational Rule for Consumers

- Consume more today if the marginal benefit of a dollar of consumption today

the marginal benefit of spending a dollar-plus-interest in the future - Combines three core principles:

- Marginal principle — should I spend one more dollar?

- Cost-benefit principle — does the benefit of spending now exceed the cost?

- Opportunity cost principle — the cost of spending now is the forgone consumption of a dollar-plus-interest in the future

- Simplified: keep spending until the marginal benefit of the last dollar of consumption is the same today as in every future period

Consumption Smoothing

- You should maintain a steady/smooth path of consumption over time, even if your income fluctuates

- Based on diminishing marginal benefit — each additional dollar of consumption yields a smaller benefit

- Moving a dollar from a time when consumption is high (low marginal benefit) to a time when consumption is low (high marginal benefit) makes you better off

- The timing of when you receive income is irrelevant — what matters is allocating consumption to whenever it yields the largest marginal benefit

Permanent Income Hypothesis

- Permanent income: your best estimate of your long-term average income over your lifetime

- People choose how much to consume based on permanent income, not current income

- e.g., a CS student with low current income but high expected future earnings has high permanent income → can afford to borrow more now

- When current income

permanent income → borrow or draw down savings (dissaving) - When current income > permanent income → save

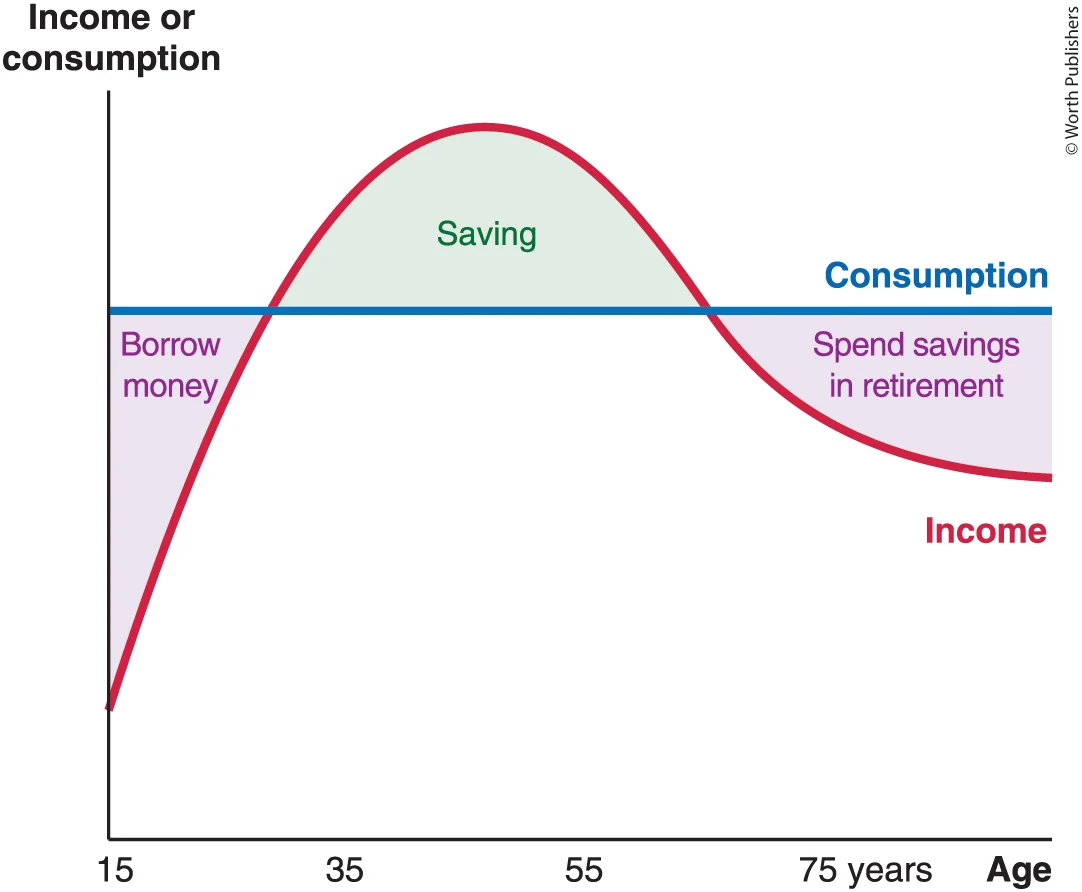

Life Cycle of Saving

- Young people: borrow (income below permanent income, e.g., students)

- Working years: save (income above permanent income, peak mid-career)

- Retirement: spend down savings (income drops again)

13.3 - The Macroeconomics of Consumption

Five Insights About Consumption and Income

- A temporary change in income → small change in consumption

- You spread the temporary gain over your lifetime (e.g., $1M lottery win → spend ~$50K/year)

- MPC out of temporary income is low (e.g., 0.05)

- A permanent change in income → large change in consumption

- A permanent raise of $50K/year means permanent income goes up by $50K → you can consume $50K more every year

- MPC out of permanent income is high, can be as high as 1

- An anticipated change in income → no change in consumption

- Your permanent income already factors in expected future changes

- e.g., a novelist who earns $80K in book years and $40K in off years just spends $60K every year

- MPC out of anticipated income = 0

- Learning about a future income change → consumption changes right away

- You respond when you get the news, not when the money arrives

- Policy implication: macro policy might have its biggest effect on consumption when announced, not when implemented

- Changes in consumption are hard to forecast

- Consumption only responds to unanticipated changes, and those are by definition hard to predict

- The level of consumption is easy to forecast (~2/3 of GDP), but changes in consumption are not

Hand-to-Mouth Consumers vs Consumption Smoothers

- Consumption smoothers: follow the Rational Rule, base spending on permanent income

- Hand-to-mouth consumers: spend their current income as they receive it, MPC = 1 for any income change regardless of type

- Caused by credit constraints (can't borrow — banks want collateral, reluctant to lend for groceries/rent) and behavioural/psychological limitations (impulse spending, failure to plan, procrastination)

Modified Insights (accounting for both types):

| Type of income change | Consumption smoothers | Hand-to-mouth | Total economy |

|---|---|---|---|

| Temporary rise | Small ↑C | Large ↑C | Intermediate ↑C |

| Permanent rise | Large ↑C | Large ↑C | Large ↑C |

| Anticipated rise | No change | Large ↑C | Intermediate ↑C |

| News of future rise | Large ↑C | No change | Intermediate ↑C |

| Forecasting changes | Hard | Look at income changes | Difficult but not impossible |

Key takeaway: the more hand-to-mouth consumers in a society, the more total consumption tracks current income rather than permanent income

13.4 - What Shifts Consumption?

Key Distinction: Movement Along vs Shift of the Consumption Function

- A change in income = movement ALONG the consumption function (not a shift)

- A change in other factors = shifts the consumption function up or down

- This distinction is important — don't mix them up on the exam

Four Consumption Shifters

1. Real Interest Rates

- Higher real interest rate → consumption function shifts down

- Lower real interest rate → consumption function shifts up

- Why it's complicated — two opposing effects:

- Substitution effect: higher interest rate raises the opportunity cost of spending now (you'd earn more by saving that dollar), so you consume less today

- Income effect: depends on whether you're a lender or borrower

- Lender: higher rates = more interest income = can consume more

- Borrower: higher rates = more interest payments = less left over to consume

- Net effect: most evidence says higher real interest rate → lower consumption

- The saving side is simpler: higher real interest rate → more saving (benefit of saving goes up)

2. Expectations

- Optimism about future economy → expect higher future income → permanent income feels higher → consumption shifts up

- Pessimism about future economy → expect lower future income → permanent income feels lower → consumption shifts down

- During COVID, consumption fell by MORE than the actual income decline because people were pessimistic → created "excess savings"

3. Taxes

- Higher taxes → lower disposable income (after-tax income) → consumption shifts down at any given level of pre-tax income/GDP

- Lower taxes → higher disposable income → consumption shifts up

- Governments sometimes use tax cuts to stimulate spending, but effectiveness depends on who gets the cut:

- Hand-to-mouth consumers → spend most of it → effective stimulus

- Consumption smoothers → recognize a temporary tax cut barely changes permanent income → save most of it → weak stimulus

4. Wealth

- Higher wealth (e.g., rising stock prices, rising house prices) → consumption shifts up

- Lower wealth (e.g., stock crash, housing crash) → consumption shifts down

- Wealth is your accumulated stock of assets minus debts — separate from income

- Housing wealth is tricky: higher house prices boost your wealth, but if you sell, you still need to buy another expensive house to live in

Summary Table

| Factor | Consumption shifts UP when... | Consumption shifts DOWN when... |

|---|---|---|

| Real interest rates | ↓ decrease | ↑ increase |

| Expectations | Optimistic | Pessimistic |

| Taxes | ↓ decrease | ↑ increase |

| Wealth | ↑ increase | ↓ decrease |

And remember: changing income does NOT shift the curve — that's a movement along it.

13.5 - Saving

Remember: Saving and consumption are two sides of the same coin — to save more you must consume less, and vice versa. So this isn't a separate topic from consumption, it's the flip side.

Four Motives for Saving

1. Changing Income Over the Life Cycle

- Income follows a hump shape: low when young → rises through 20s/30s → peaks in 40s/50s → drops at retirement

- Consumption smoothing means you borrow when young, save in midlife, spend down savings in retirement

- Macro implication: demographics affect national savings

- More old/young people in the population → lower national savings (they're dissaving or borrowing)

- Canada's 65+ population has more than doubled in recent decades → national savings rate has dropped to ~3%

2. Changing Needs Over the Life Cycle

- Your needs aren't constant — they change as life stages change (tuition → student loans → wedding → kids → childcare costs etc.)

- You should save more when your needs are low so you can spend more when needs are high

- This isn't contradicting consumption smoothing — the Rational Rule says spend more when the marginal benefit of spending is higher, and some life stages genuinely have higher marginal benefits

- Practical takeaway: even if your permanent income allows higher consumption in your early 20s, it's smart to spend modestly because expenses will likely rise in your 30s

3. Bequests

- Some people save to leave wealth behind when they die — to children, charity, or a cause they care about

- Explains why many elderly people don't fully spend down their wealth in retirement

4. Precautionary Saving

- Saving for a rainy day — building a buffer stock of savings in case of financial emergencies (layoff, medical emergency, unexpected costs)

- ~43% of Canadian workers would find it difficult to cope if their paycheque was delayed by just one week — almost half are living paycheque to paycheque

- Financial planners recommend a buffer of 3-6 months of typical consumption

- Macro implication: when economic uncertainty rises → precautionary saving rises → consumption falls

- This is exactly what happened during COVID — savings rate soared not just because people couldn't go out, but because uncertainty made people cut spending as a precaution

- Government support payments also added to the savings buildup

Smart Saving Strategies (worth knowing conceptually)

- Set a budget in advance and stick to it — people make better decisions when planning ahead vs. deciding in the moment (chocolate vs. apple experiment)

- Build a rainy-day fund BEFORE making extra payments on student loans — you need liquidity in case of emergencies

- Sign up for your employer's retirement plan immediately — especially if they match contributions (that's free money)

- Plan to save out of future income — easier than cutting current consumption (e.g., when student loans are paid off, redirect those payments to retirement savings)

- Avoid high fees on investment accounts and high-interest debt (especially credit cards and payday loans)

- Payday loans: annual interest rates often over 100%, sometimes over 1,000% — avoid these

Questions

- Consider a consumption function of the following form: C = 50 + (0.75)Y. If disposable income is equal to 500, what is the average propensity to save (fraction of income that is saved)?

0.15. Just plug income in, find savings and then get the rate - If the Jones family's disposable income increases from $1200 to $1700 and their desired saving increases from -$100 to +$100, then the family's

Delta income = +500. Delta save = +200 which means delta consume = +300

And then MPC is just 300 / 500 by definition which is obviously 0.6. - Which of the following would be likely to cause an increase in both current consumption and current savings?

An increase in current income.